Key Findings

- One of the central achievements of the TaxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. Cuts and Jobs Act (TCJA) of 2017 was to enhance US economic competitiveness by implementing the largest corporate tax reform in a generation. Studies indicate TCJA’s corporate tax reforms substantially raised US capital investment and economic growth.

- Several provisions of TCJA expanded the corporate tax baseThe tax base is the total amount of income, property, assets, consumption, transactions, or other economic activity subject to taxation by a tax authority. A narrow tax base is non-neutral and inefficient. A broad tax base reduces tax administration costs and allows more revenue to be raised at lower rates. , which as a share of GDP grew by 56 percent in the five years following TCJA enactment, from a pre-TCJA average of 7.1 percent of GDP to 11.1 percent of GDP in 2022.

- Additionally, the InflationInflation is when the general price of goods and services increases across the economy, reducing the purchasing power of a currency and the value of certain assets. The same paycheck covers less goods, services, and bills. It is sometimes referred to as a “hidden tax,” as it leaves taxpayers less well-off due to higher costs and “bracket creep,” while increasing the government’s spending power. Reduction Act (IRA) of 2022 levied new taxes on corporate income, including the corporate alternative minimum tax (CAMT), the 1 percent excise taxAn excise tax is a tax imposed on a specific good or activity. Excise taxes are commonly levied on cigarettes, alcoholic beverages, soda, gasoline, insurance premiums, amusement activities, and betting, and typically make up a relatively small and volatile portion of state and local and, to a lesser extent, federal tax collections. on stock buybacks, and several green energy tax credits.

- Corporate tax revenue now exceeds pre-TCJA levels, both as a share of GDP and as a share of all federal tax collections. However, lawmakers may roll back some of the TCJA’s base broadeners that are a drag on economic growth, such as the requirement to amortize research and development costs.

- Lawmakers may be considering raising corporate taxes in other ways to offset the budgetary cost of extending expiring provisions of the TCJA and implementing other tax cuts. Three such corporate tax hikes that have been discussed are: (1) new limits on corporate state and local tax (C-SALT) deductions, (2) an expansion of current limits on public companies’ compensation deductions under Section 162(m), and (3) an increase of the stock buyback excise tax above the current 1 percent level. Of these three, the House Ways & Means legislation only included changes to 162(m); however, in recognition that some combination of the three could be included in any final version enacted into law, this paper examines their potential impact. We found that, depending on how they are structured, each tax increase could reduce long-run GDP and American incomes by more than 0.1 percent and reduce hours worked by more than 60,000 full-time equivalent (FTE) jobs.

- Additionally, an expansion of 162(m) and an increase in the stock buyback tax—both of which currently target only publicly-traded companies—could incentivize public companies to go private and disincentivize private companies from going public. This could reduce retail investors’ returns and prevent less-affluent investors from accessing quality investment opportunities, disproportionately harming lower-income Americans. This is particularly problematic given that stock and bond ownership (either directly or through retirement accounts) make up nearly half the financial assets of the bottom 50 percent of Americans by net wealth.

- As lawmakers consider options for budgetary offsets, they should prioritize competitiveness and economic growth, as a heavier corporate tax burden will undermine the core purpose and achievement of the TCJA.

Introduction

At the end of 2025, and absent congressional action, much of the federal tax code will expire and snap back to the higher tax rates that prevailed prior to the Tax Cuts and Jobs Act (TCJA) of 2017. Lawmakers are considering how to extend the TCJA’s expiring provisions and enact other tax cuts while dealing with a massive debt overhang from years of spending in excess of revenues and a daunting fiscal trajectory even in the absence of additional tax cuts. House members are considering draft legislation from the Ways and Means CommitteeThe Committee on Ways and Means, more commonly referred to as the House Ways and Means Committee, is one of 29 U.S. House of Representative committees and is the chief tax-writing committee in the U.S. The House Ways and Means Committee has jurisdiction over all bills relating to taxes and other revenue generation, as well as spending programs like Social Security, Medicare, and unemployment insurance, among others. while the Senate is developing its own bill that will need to be reconciled with the House version before enactment.[1] While most of the expiring provisions and potential tax cuts relate to individual income, several business provisions are being considered, both tax cuts and revenue raisers.

Understanding how the TCJA changed the corporate tax rate and tax base can level-set the current congressional debate and illustrate what past changes mean for tax reform going forward. One of the central purposes of the TCJA was to enhance US competitiveness and increase economic growth by lowering the corporate tax rate, which was the highest in the developed world, and reforming our antiquated international tax code that disadvantaged US multinational enterprises (MNEs) relative to peers based in other countries.

The old tax code suppressed corporate investment and encouraged a variety of tax planning techniques to avoid the US corporate tax, including profit shiftingProfit shifting is when multinational companies reduce their tax burden by moving the location of their profits from high-tax countries to low-tax jurisdictions and tax havens. and corporate inversions that shrank the corporate tax base.[2] By reducing the corporate tax rate, reforming international taxes, and broadening the corporate tax base, the TCJA improved competitiveness, leading to stronger economic growth, higher profits, and, more recently, corporate tax collections that are at or above pre-TCJA levels.[3] However, lawmakers may roll back some of the TCJA’s base broadeners that are a drag on economic growth, such as the requirement to amortize research and development (R&D) costs, which would boost growth and investment in the long run while reducing the corporate tax base and revenues in the short run.

Lawmakers may be considering raising corporate taxes in other ways to offset the budgetary cost of extending expiring provisions of the TCJA and implementing other tax cuts, such as by curtailing deductions for corporate state and local taxes and executive compensation and by increasing the stock buyback tax. These changes would reduce competitiveness and economic growth, undermining the core purpose and achievement of the TCJA.

Corporate Tax Changes Made Under the TCJA and IRA

In 2017, Republicans enacted the TCJA, which lowered the federal corporate tax rate from 35 percent to 21 percent. The lower rate put the US roughly in the middle of the pack of developed countries after accounting for state and other subnational corporate taxes. The TCJA also reformed the international tax code, replacing the old system of worldwide taxation and deferral of foreign profits with a hybrid territorial regime that avoided penalizing companies for bringing foreign profits home. To address lingering concerns about companies shifting profits offshore, the TCJA introduced a new regime of minimum taxes on foreign income, including global intangible low-taxed income (GILTI), foreign-derived intangible income (FDII), and base erosion and anti-abuse tax (BEAT).

The international reforms effectively broadened the corporate tax base to include a greater share of foreign income. Several other changes broadened the corporate tax base for both domestic corporations and MNEs. The TCJA’s major base broadeners included limitations on deductions for net interest expense, net operating losses, and fringe benefits; a new requirement to amortize research and development expenses over 5 or 15 years; and the repeal of the domestic production activities deduction. In total, the Joint Committee on Taxation (JCT) estimated the offsets would raise more than $1 trillion over a decade, paying for more than three-quarters of the $1.3 trillion revenue loss from reducing the corporate tax rate.[4]

The TCJA reforms also changed the timing of tax collections, shifting them out into the future. For example, the policy of 100 percent bonus depreciationBonus depreciation allows firms to deduct a larger portion of certain “short-lived” investments in new or improved technology, equipment, or buildings in the first year. Allowing businesses to write off more investments partially alleviates a bias in the tax code and incentivizes companies to invest more, which, in the long run, raises worker productivity, boosts wages, and creates more jobs. , which applied from 2018 to 2022 before phasing out beginning in 2023, shifted forward deductions for capital investment. In 2022, business taxes went up as R&D amortization and a more severe interest limitation took effect. JCT estimated that the TCJA’s business and international reforms would reduce revenue initially but raise revenue on net by 2023, with a net revenue gain of $21 billion in 2024. Tax Foundation modeling found similar results.[5]

The TCJA reforms also boosted investment and corporate profits while encouraging companies to report more profits for tax purposes. The original JCT score was static, so it did not include impacts of economic growth, but it did estimate how companies would shift reporting of profits to domestic sources for tax purposes. In 2018, the Congressional Budget Office (CBO) estimated the TCJA would boost economic growth and the corporate profits tax base considerably, as did we.[6] Studies indicate the TCJA boosted business investment for firms with tax cuts over the first few years of the TCJA’s enactment.[7]

The Inflation Reduction Act (IRA) of 2022 also altered corporate taxes in several ways. The IRA introduced a new 15 percent corporate alternative minimum tax (CAMT) for corporations earning over $1 billion of profits, with the tax applying to a new base of adjusted financial statement income. The IRA also introduced a new 1 percent excise tax on net share repurchases (buybacks) by publicly traded companies as well as several green energy tax credits. While these provisions went into effect in 2023, the complexity of the statute and subsequent tax regulations issued by the Treasury and the IRS led to delayed implementation of the CAMT and buyback tax and increased cost estimates for the tax credits, making the net impact on corporate tax revenue difficult to assess but likely negative.[8]

Impact on the Corporate Tax Base and Revenue

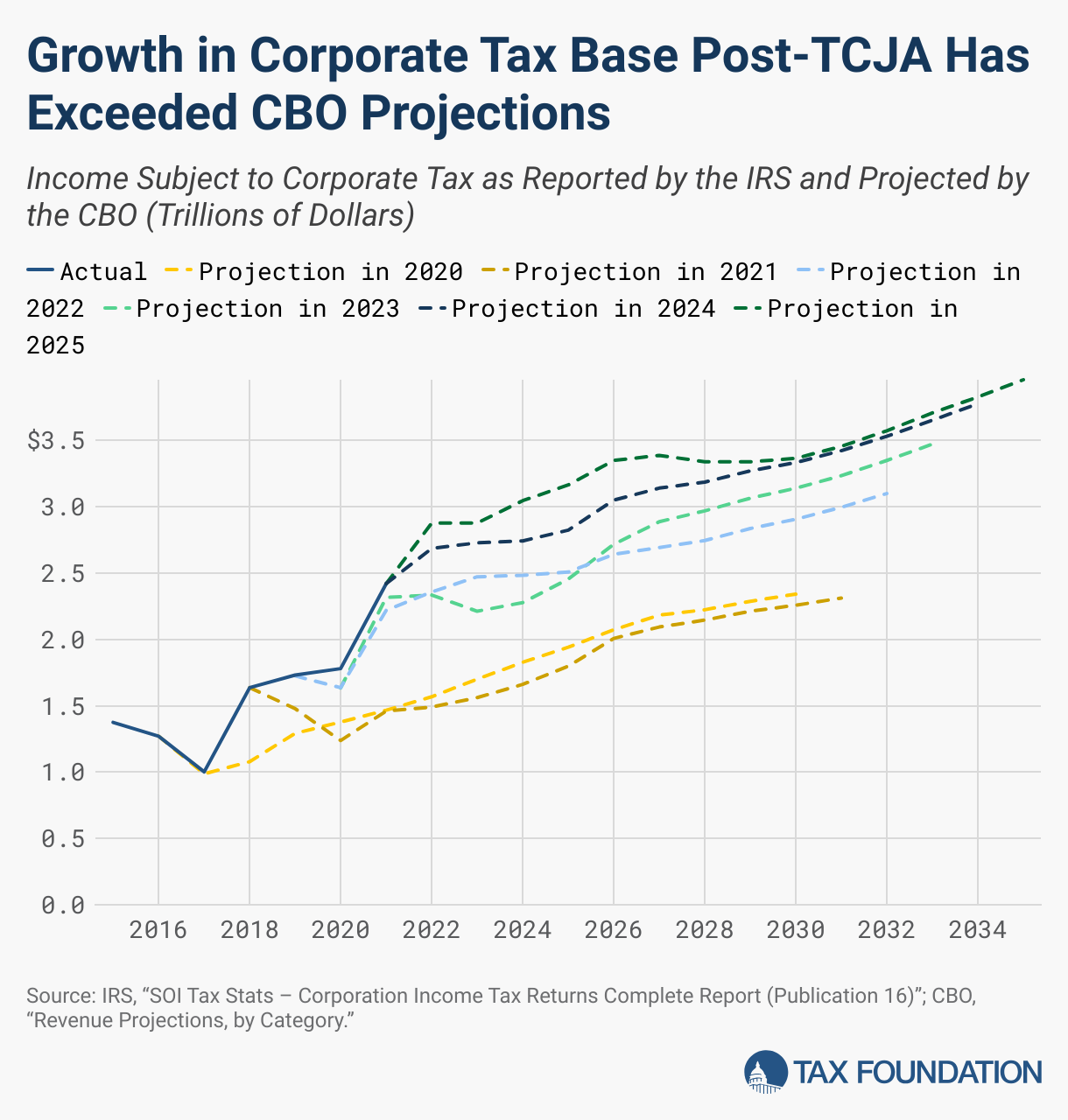

CBO produces a measure of the corporate tax base derived from IRS data, which generally matches the IRS measure of “income subject to tax” for C corporations with actual values available through 2021 and CBO projections available through 2035.[9]

In 2018, the first year after the TCJA was enacted, the corporate tax base grew 63 percent, from about $1 trillion in 2017 to $1.6 trillion in 2018. The corporate tax base continued to grow in subsequent years, due in part to the phase-in of TCJA offsets, namely R&D amortization and the stricter limitation on interest deductions that went into effect in 2022 and the phase-down of bonus depreciationDepreciation is a measurement of the “useful life” of a business asset, such as machinery or a factory, to determine the multiyear period over which the cost of that asset can be deducted from taxable income. Instead of allowing businesses to deduct the cost of investments immediately (i.e., full expensing), depreciation requires deductions to be taken over time, reducing their value and discouraging investment. beginning in 2023. Additionally, post-pandemic inflation and economic growth have contributed to higher revenues. By 2022, the corporate tax base reached $2.9 trillion and by 2024, it exceeded $3 trillion, more than tripling since 2017 before accounting for inflation, according to CBO estimates.

The corporate tax base fluctuates because of policy changes, the business cycle, and inflation, with the outbreak of high inflation beginning in 2021 substantially complicating our analysis. A more useful measure over time is the corporate tax base as a share of GDP, which effectively controls for inflation. In Figure 1, this measure is shown over the 20 years prior to the TCJA (1998-2017) and through 2035 according to CBO projections.

In the 20 years prior to TCJA, the corporate tax base averaged 7.1 percent of GDP, dropping to its lowest level in 2017, at 5.1 percent. In 2018, it jumped to 7.9 percent of GDP and continued to climb in subsequent years to 11.1 percent of GDP in 2022—far exceeding the corporate tax base in any year leading up to the TCJA. Thus, in the five years following TCJA enactment, after most but not all base broadeners had taken effect, the corporate tax base as a share of GDP grew 56 percent over its pre-TCJA average of 7.1 percent.

In subsequent years, CBO projects the corporate tax base falls to 10.4 percent of GDP in 2023, rises briefly in 2026 to 10.6 percent, and then falls steadily from there to 8.9 percent of GDP in 2035.[10] This reflects both CBO’s projection of corporate profits, which is highly uncertain, as well as the timing effects of major base broadeners, including R&D amortization and stricter limits on interest deductions that began in 2022, the phase-out of bonus depreciation that began in 2023, and higher tax rates on the TCJA’s international provisions (GILTI, FDII, and BEAT) that will begin in 2026. Lawmakers are considering altering many of these provisions, likely rolling back R&D amortization and other base broadeners to some degree.

CBO’s projections of the corporate tax base have undershot actuals since the TCJA was enacted, including in the years prior to the unexpected inflation that began in 2021. For example, in their 2020 publication (the first year CBO made this data available), CBO underestimated the actual corporate tax base by 34 percent in 2018 and by 25 percent in 2019. The increase in reported profits subject to tax suggests the TCJA changed corporate tax planning and avoidance behavior, providing an additional boost to the corporate tax base above economic growth, inflation, and the TCJA’s base broadeners described above (such as limits on deductions for interest expense). Over the next decade, CBO projects the corporate tax base will average 9.6 percent of GDP from 2025 to 2034—a 35 percent increase over the pre-TCJA average.[11]

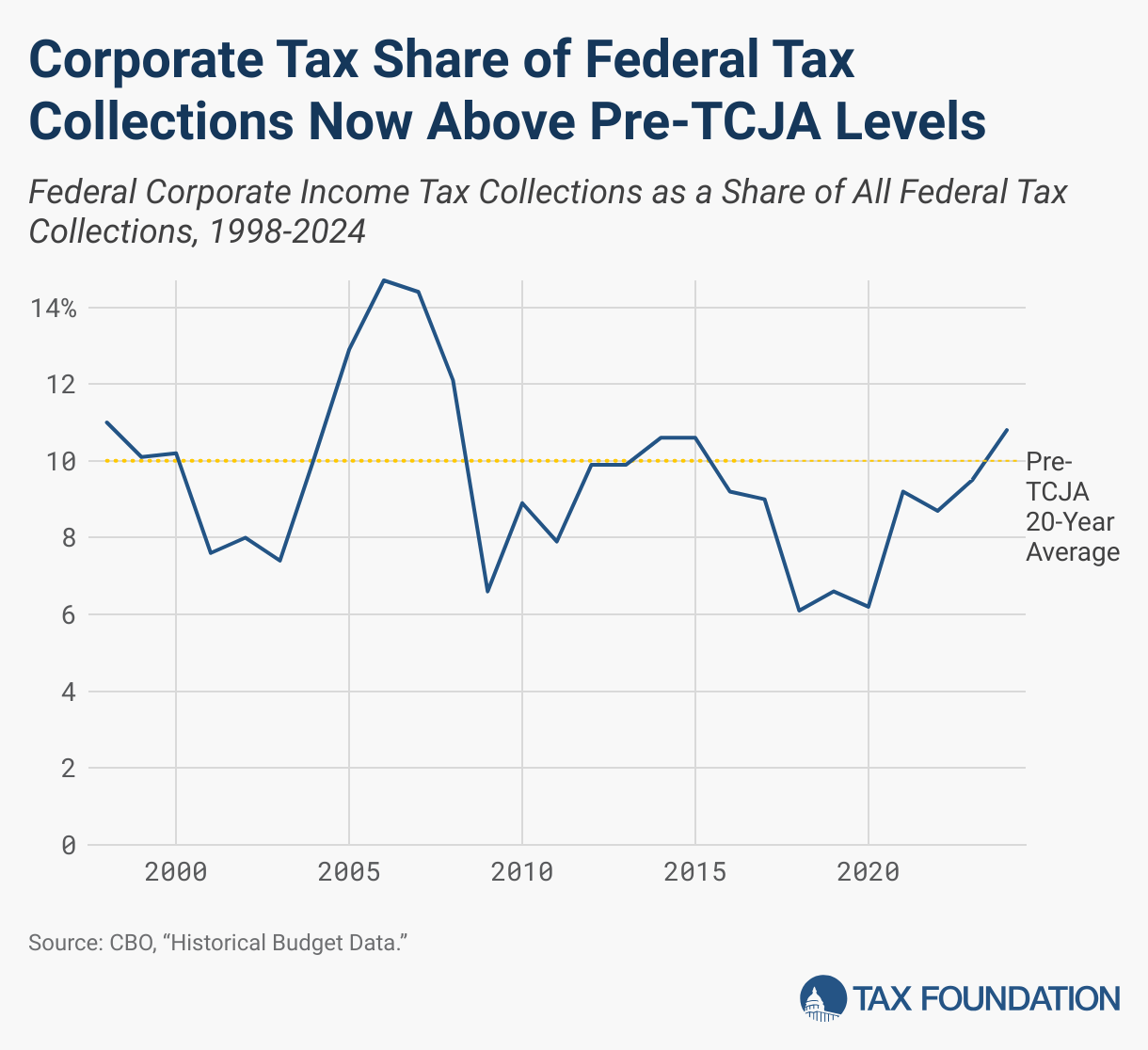

Actual corporate tax revenue, which is reported on a more timely basis, provides corroborating evidence that the corporate tax base has expanded since the TCJA’s enactment.[12] Federal corporate tax collections have been on an upswing generally since 2020, owing primarily to a rebound in the economy and profits since the pandemic and secondarily to tax policy changes, including the phase-in of TCJA base broadeners and the IRA’s CAMT, buyback tax, and energy credits. As a share of GDP, corporate tax collections reached about 1.8 percent in fiscal year 2024, the highest level since 2015 and above the 1.7 percent average over the 20 years prior to the TCJA. Corporate tax collections can vary from one year to the next due to timing shifts and other factors, and when averaged over the last two years corporate tax collections are roughly on par with the pre-TCJA average.[13]

Other measures indicate corporate tax collections are at or above historical levels. Corporate tax collections were 10.8 percent of all federal tax collections in fiscal year 2024, the highest share since 2008.[14] On average over the last two years, corporate tax collections were 10.1 percent of all federal tax collections—higher than the 10 percent average over the 20 years prior to the TCJA.

Going forward, CBO projects a decline in corporate tax revenue as a share of GDP to 1.2 percent by 2034. This is a larger decline than CBO projects for the corporate tax base, reflecting, in part, revenue losses from the IRA energy tax credits.[15]

Potential Corporate Tax Hikes and Other Changes

To offset the budgetary costs of extending the TCJA and enacting other tax cuts, lawmakers may be considering further increases to the corporate tax burden that are distortionary and fundamentally unsound, including by curtailing deductions for state and local taxes and executive compensation and by increasing the tax on stock buybacks.

Lawmakers are contemplating putting new limits on corporate state and local tax (C-SALT) deductions in an apparent attempt to extend the current cap on SALT deductions that applies to individuals.[16] This ignores the fact that the corporate income taxA corporate income tax (CIT) is levied by federal and state governments on business profits. Many companies are not subject to the CIT because they are taxed as pass-through businesses, with income reportable under the individual income tax. is different from the individual income taxAn individual income tax (or personal income tax) is levied on the wages, salaries, investments, or other forms of income an individual or household earns. The U.S. imposes a progressive income tax where rates increase with income. The Federal Income Tax was established in 1913 with the ratification of the 16th Amendment. Though barely 100 years old, individual income taxes are the largest source of tax revenue in the U.S. in at least two important ways. First, the corporate tax applies to profits, which allows deductions for legitimate business costs. Second, one of the key rationales for the SALT cap for individuals is it reduces subsidies for high-tax states, but for businesses operating across state lines, this effect is greatly reduced due to rules that apportion income taxes by the location of sales.[17]

Limiting C-SALT deductions could raise substantial amounts of tax revenue but would do so by increasing marginal tax rates on corporate investment, with the largest burden falling on manufacturing. The revenue and economic impacts depend on which state and local taxes are disallowed, with possibilities including corporate income, property, sales, excise, and severance taxes. We estimate that repealing C-SALT deductions for corporate income taxes alone would raise about $209 billion over the next decade, conventionally measured, but would reduce long-run GDP and wages by 0.1 percent, shrink the capital stock by 0.2 percent, and reduce hours worked by 28,000 full-time equivalent jobs. Accounting for lower economic output reduces the revenue gain to $154 billion over the next decade.

Going further and disallowing C-SALT deductions for property taxes would raise about $432 billion over the next decade on a conventional basis but would reduce long-run GDP by 0.6 percent, shrink the capital stock by 1.1 percent, lower wages by 0.5 percent, and reduce hours worked by 156,000 full-time equivalent jobs. Revenue gains on a dynamic basis would fall to $124 billion.[18]

Limiting C-SALT deductions would also reduce the competitiveness of US-based companies relative to peers based in other countries. The current statutory combined federal-state corporate income tax rate in the US is about 25.6 percent, roughly on par with countries in the Organisation for Economic Co-operation and Development (OECD); the US is above the simple average rate but below the average rate weighted by GDP among OECD countries.[19] Disallowing C-SALT for corporate income taxes would raise the US combined rate by about 1.2 percentage points, putting the US above the OECD weighted average. Many but not all countries disallow deductions for subnational income taxes, but only a few extend this disallowance to property and other taxes.[20]

Table 1: Long-Run Economic and Budget Window Revenue Impacts of Potential Corporate Tax Increases

| GDP | GNP | Capital Stock | Wages | Hours Worked Converted to Full-time Equivalent Jobs | Static Tax Revenue 2025-2034 (Billions of Dollars) | Dynamic Tax Revenue 2025-2034 (Billions of Dollars) | |

|---|---|---|---|---|---|---|---|

| Disallow corporate SALT deductions for corporate income tax | -0.1% | -0.1% | -0.2% | -0.1% | -28,000 | $209.4 | $154.1 |

| Disallow corporate SALT deductions for corporate income and property tax | -0.6% | -0.5% | -1.1% | -0.5% | -156,000 | $432.3 | $123.8 |

| Expand Secion 162(m) limitations on corporate executive compensation | -0.1% | -0.1% | -0.2% | 0% | -169,000 | $255.5 | $147.0 |

| Increase stock buyback tax to 4% | -0.2% | -0.2% | -0.4% | -0.2% | -63,000 | $241.9 | $147.6 |

Source: Tax Foundation General Equilibrium Model, April 2025

Lawmakers are also considering expanding the current limits on deductions for corporate executive compensation.[21] First enacted in 1993, Section 162(m) disallows deductions above $1 million for compensation of certain top executives of publicly traded companies. As part of the Affordable Care Act, the Obama administration implemented a lower threshold of $500,000 that applies to health insurance executives. The TCJA expanded 162(m) to include performance-based pay and required that once an individual is a covered employee, they are always a covered employee.

The American Rescue Plan Act of 2021 expanded the definition of covered employees so that by 2027 it will apply to the CEO, CFO, and the next eight most highly compensated employees. The Biden administration proposed expanding 162(m) further to include all employees of C corporations, whether publicly held or privately held, who earn more than $1 million, and “closing some mechanisms taxpayers have used in an attempt to avoid the deduction limitation” such as use of affiliated partnerships.[22] Regulations proposed in the final days of the Biden administration would also tighten up the affiliation and aggregation rules to include controlled foreign corporations (CFCs).[23] Legislation under consideration by the House Ways and Means Committee would similarly tighten aggregation rules.[24]

Section 162(m) is fundamentally arbitrary and non-neutral as it applies high tax rates to a select few employees in certain types of businesses. While the TCJA reduced the federal corporate tax rate to 21 percent and the top individual tax rate to 37 percent, the combination under 162(m) subjects corporate executive compensation to a top marginal tax rateThe marginal tax rate is the amount of additional tax paid for every additional dollar earned as income. The average tax rate is the total tax paid divided by total income earned. A 10 percent marginal tax rate means that 10 cents of every next dollar earned would be taken as tax. of 58 percent at the federal level (the 37 percent top marginal individual income tax rate plus the 21 percent corporate income tax rate), and with state income taxes the top rate can exceed 70 percent.[25]

Such high and non-neutral tax rates naturally lead to avoidance, tax planning, and other distortions, including outsourcing to contractors and offshoring to CFCs. Expanding the reach of 162(m) to include privately held companies, affiliated companies, and contractors, as proposed by the Biden administration, could perversely cause more extensive and complicated tax planning around the provision. For instance, US public companies subject to a more punitive version of 162(m) may be incentivized at the margin to shift hiring offshore, outsource a greater share of management functions, or engage in other distortionary actions, perhaps through implementing more opaque compensation packages, contracting, relabeling, and even corporate inversions.

Additionally, a beefed-up 162(m) would put US companies at a competitive disadvantage relative to peers operating in other countries that have no such rules.[26] In particular, it would make US companies less able to hire and retain the world’s top talent in management functions as well as in other areas, such as computer science, artificial intelligence development, medical innovation, or other in-demand fields.

Expanding limits on business compensation deductibility would also have far-reaching effects across the US economy. We estimate the Biden budget proposal to expand 162(m) would reduce long-run GDP and the capital stock by more than 0.1 percent, and reduce hours worked by 169,000 full-time equivalent jobs. While we estimate it would raise about $256 billion over the next decade on a conventional basis, accounting for lower economic output reduces that gain to $147 billion. Revenue might be further reduced to the extent companies plan around the tax, for example, through corporate inversions, foreign acquisitions of US companies, and other erosions of the corporate tax base. It would also weigh on US shareholders and retirement accounts, which rely heavily on the health and future earnings growth of US publicly traded companies. This would disproportionately negatively affect low-income Americans, given that stock and bond ownership make up nearly half of the financial assets of the bottom 50 percent of Americans households by wealth.[27]

Even without any expansion of 162(m), because the $1 million threshold is unadjusted for inflation and because of the “once covered, always covered” rule, every year more employees and companies are affected. A Treasury analysis of pre-TCJA law indicated a growing impact of the provision, with the number of US companies affected increasing from 725 in 2005 (about 14 percent of publicly traded companies) to 1,185 in 2013 (about 27 percent of publicly traded companies).[28] Rather than expanding 162(m), lawmakers should repeal it entirely.

A third corporate tax hike that may be under consideration, which would further target and disadvantage US publicly traded companies, is an expansion of the current 1 percent tax on stock repurchases, i.e., buybacks. Stock buybacks are one of the ways businesses return value to their shareholders. Companies can return earnings to shareholders by issuing dividends (namely cash payments) or with stock buybacks (purchasing shares of their own company). US shareholders are subject to tax on dividends received and capital gains realized, which represent a second layer of tax on corporate income after entity-level taxes. Accounting for both layers of tax, the corporate integrated tax rate in the US exceeds 47 percent for corporate income distributed as either capital gains or dividends, which is well above average among OECD and EU countries.[29] For corporate income distributed as capital gains, 32 OECD and EU countries have a lower integrated tax rate than the US. This competitive disadvantage would be worsened and made more distortionary by increasing the buyback tax.

Taxing buybacks penalizes a corporate financing option that supports a dynamic economy and benefits retail investors. As much as 95 percent of the money returned to shareholders from stock buybacks subsequently gets reinvested in other public companies.[30] As well, stock buybacks enable investors to fund smaller firms and start-ups where the opportunities for growth and innovation can be much greater than those of established firms. A higher buyback tax would distort this efficient and beneficial process of recycling investable funds.[31] While some have argued that the buyback tax reduces the tax advantage of buybacks over dividends, it creates the reverse bias for tax-exempt shareholders (who own, for example, tax-advantaged retirement accounts), worsens the bias against investment financed by equity versus debt, and disproportionately penalizes investment in equipment and other short-lived assets.[32]

We estimate that increasing the buyback tax to 4 percent, as proposed by the Biden administration, would raise substantial revenue: $242 billion over the next decade on a conventional basis. However, it would reduce long-run GDP and wages by 0.2 percent, shrink the capital stock by 0.4 percent, and reduce hours worked by 63,000 full-time equivalent jobs. After accounting for reduced economic growth, a higher buyback tax would raise $148 billion over the next decade. A better approach would be to eliminate this tax altogether.[33]

Conclusion

The TCJA put an end to corporate inversions and other distortionary and inefficient tax planning by addressing what was then an uncompetitive corporate tax code. The TCJA’s lower corporate tax rate and base broadeningBase broadening is the expansion of the amount of economic activity subject to tax, usually by eliminating exemptions, exclusions, deductions, credits, and other preferences. Narrow tax bases are non-neutral, favoring one product or industry over another, and can undermine revenue stability. have led to corporate tax revenues in recent years that are on par with pre-TCJA levels. However, some of the TCJA’s base broadeners penalize investment and will detract from economic growth if left unaddressed, such as the requirement to amortize R&D costs.

As lawmakers now consider how to extend the expiring TCJA provisions while reducing the budgetary cost, they should not backtrack on the TCJA’s progress in improving the competitive position of US companies. The world continues to compete for corporate investment and if the US is to retain its leadership position, the corporate tax must be streamlined and made less distortionary, not more. One promising avenue is to increase immediate expensing of capital investment for R&D, equipment, and other assets, which lawmakers may be considering as part of reconciliation.

Lawmakers are right to be concerned about deficits and the perilous fiscal trajectory of the federal government. However, raising distortionary taxes on US businesses—with disproportionate impacts on publicly traded companies—would be counterproductive to addressing the problem, as it would undermine long-run growth, diminishing wages and other income that comprise the vast majority of the federal government’s tax base. It would also harm retail investors and retirement savers invested in the public markets. Rather, lawmakers should rein in spending growth to align it with historical levels. That includes reducing the increasing prevalence of spending through the tax code, e.g., on refundable tax credits, a large portion of which are counted as outlays.[34]

Lawmakers can both improve long-run economic growth and put the federal government’s fiscal trajectory on a more sustainable course, but it requires following a narrow path that avoids unforced errors, usual political tendencies, and populist rhetoric. While not well understood by most voters, US corporations currently pay substantial amounts of tax, in line with pre-TCJA levels mainly because of the base broadeners included in the law. Rather than raising corporate taxes and cluttering up the corporate tax code with more complex features and barriers to investment, lawmakers should recognize the vital importance to the economy of getting corporate taxes right—building on the progress made with the TCJA—keeping them as competitive, simple, and conducive to investment as possible.

Stay informed on the tax policies impacting you.

Subscribe to get insights from our trusted experts delivered straight to your inbox.

SubscribeReferences

[1] US House Committee on Ways and Means, “Full Committee Markup of Legislative Proposals to Comply with the Reconciliation Directive Included in Section 2001 of the Concurrent Resolution on the Budget for Fiscal Year 2025, H. Con. Res. 14.,” May 13, 2025, https://waysandmeans.house.gov/event/full-committee-markup-of-legislative-proposals-to-comply-with-the-reconciliation-directive-included-in-section-2001-of-the-concurrent-resolution-on-the-budget-for-fiscal-year-2025-h-con-res-14/.

[2] Congressional Budget Office, “An Analysis of Corporate Inversions,” September 2017, https://www.cbo.gov/system/files/115th-congress-2017-2018/reports/53093-inversions.pdf; Bloomberg, “Tracking Tax Runaways,” Mar. 1, 2017, https://www.bloomberg.com/graphics/tax-inversion-tracker/.

[3] William McBride, “Another Huge Federal Deficit in Fiscal Year 2024 Despite Surging Corporate and Other Tax Collections,” Tax Foundation, Oct. 10, 2024, https://taxfoundation.org/blog/federal-budget-deficit-tcja-revenue-spending/.

[4] Joint Committee on Taxation, “Estimated Budget Effects of the Conference Agreement for H.R. 1, the ‘Tax Cuts and Jobs Act,’” JCX-67-17, Dec. 18, 2017, https://www.jct.gov/publications/2017/jcx-67-17/.

[5] Tax Foundation, “Preliminary Details and Analysis of the Tax Cuts and Jobs Act,” Dec. 18, 2017, https://taxfoundation.org/research/all/federal/final-tax-cuts-and-jobs-act-details-analysis/.

[6] Congressional Budget Office, “The Budget and Economic Outlook: 2018 to 2028,” Apr. 9, 2018, https://www.cbo.gov/publication/53651.

[7] William McBride and Alex Durante, “New Study Finds TCJA Strongly Boosted Corporate Investment,” Tax Foundation, Oct. 31, 2023, https://taxfoundation.org/blog/tcja-corporate-tax-economic-effects/.

[8] William McBride, Alex Muresianu, Erica York, and Michael Hartt, “Inflation Reduction Act One Year After Enactment,” Tax Foundation, Aug. 16, 2023, https://taxfoundation.org/research/all/federal/inflation-reduction-act-taxes/.

[9] However, for 2018, there is a substantial difference between IRS and CBO data, as CBO excludes from the corporate tax base deemed repatriationRepatriation is the process by which multinational companies bring overseas earnings back to the home country. Prior to the 2017 Tax Cuts and Jobs Act (TCJA), the US tax code created major disincentives for US companies to repatriate their earnings. Changes from the TCJA eliminate these disincentives. from previously untaxed foreign profits, amounting to $320 billion, which is subject to the section 965 one-time transition tax as part of the TCJA. Other measures of the corporate tax base provided by CBO and IRS produce similar results as presented in this section, such as a measure called “Net Income (Less deficit) for Corporations Subject to the Corporate Income Tax,” which includes net operating losses among other items. See Congressional Budget Office, “Revenue Projections, by Category,” https://www.cbo.gov/data/budget-economic-data#7; Internal Revenue Service Statistics of Income, “SOI Tax Stats – Corporation Income Tax Returns Complete Report (Publication 16),” https://www.irs.gov/statistics/soi-tax-stats-corporation-income-tax-returns-complete-report-publication-16.

[10] As mentioned, actual values for “income subject to tax” are only available through 2021, requiring projections beyond that date.

[11] The official estimates of corporate tax expenditures provide an alternative perspective on the corporate tax base, generally corroborating the results shown here by indicating a reduction in corporate tax expenditures in the years following the TCJA and a subsequent rise in the years following the IRA. See Alex Muresianu, “JCT Report Shows How Corporate Tax Breaks have Expanded,” Tax Foundation, Jan. 18, 2024, https://taxfoundation.org/data/all/federal/tax-expenditures-pre-post-tcja/.

[12] Congressional Budget Office, “Historical Budget Data,” https://www.cbo.gov/data/budget-economic-data#2.

[13] This is consistent with JCT estimates indicating TCJA business and international changes would on net raise revenue by 2023.

[14] This was not the result of other revenue sources dropping. Federal tax collections overall in fiscal year 2024 were 17.1 percent of GDP, roughly matching the average over the 20 years prior to the TCJA. See William McBride, “Another Huge Federal Deficit in Fiscal Year 2024 Despite Surging Corporate and Other Tax Collections,” Tax Foundation, Oct. 10, 2024, https://taxfoundation.org/blog/federal-budget-deficit-tcja-revenue-spending/.

[15] Congressional Budget Office, “The Budget and Economic Outlook: 2025 to 2035,” Jan. 2025, https://www.cbo.gov/publication/61172; Congressional Budget Office, “The Budget and Economic Outlook: 2024 to 2034,” Feb. 2024, https://www.cbo.gov/publication/59946.

[16] Benjamin Guggenheim, “Ways and Means Eyeing Limits to Corporate Tax Deductions,” Politico, Feb. 18, 2025, https://www.politico.com/live-updates/2025/02/18/congress/corporate-tax-deductions-00204736. While not in the current draft legislation being considered by the House Ways and Means Committee, new limitations on C-SALT deductions could become part of legislation as part of the reconciliation process.

[17] Jared Walczak and Garrett Watson, “Congressional Policymakers Should Tread Carefully When Weighing New Corporate SALT Deduction Limits,” Tax Foundation, Mar. 3, 2025, https://taxfoundation.org/blog/corporate-tax-deduction-c-salt/.

[18] Eliminating deductions for entity-level pass-through taxes (workarounds) would raise additional revenue but would also increase the economic damage. See Garrett Watson and Daniel Bunn, “Growth Should Be a Key Consideration if Corporate SALT Is Limited,” Tax Foundation, Mar. 24, 2025, https://taxfoundation.org/blog/corporate-salt-deduction-limitation/.

[19] Cristina Enache, “Corporate Tax Rates Around the World, 2024,” Tax Foundation, Dec. 17, 2024, https://taxfoundation.org/data/all/global/corporate-tax-rates-by-country-2024/.

[20] Garrett Watson and Daniel Bunn, “Growth Should Be a Key Consideration if Corporate SALT Is Limited,” Tax Foundation, Mar. 24, 2025, https://taxfoundation.org/blog/corporate-salt-deduction-limitation/.

[21] Richard Rubin and Olivia Beavers, “GOP Weighs More Taxes on Companies for Top Executives’ Pay,” The Wall Street Journal, Apr. 30, 2025, https://www.wsj.com/politics/policy/gop-weighs-more-taxes-on-companies-for-top-executives-pay-16d72a17.

[22] Department of the Treasury, “General Explanations of the Administration’s Fiscal Year 2025 Revenue Proposals,” Mar. 11, 2024, https://home.treasury.gov/system/files/131/General-Explanations-FY2025.pdf.

[23] RSM, “IRS Proposes Regulations to Implement Changes to Section 162(m),” Jan. 29, 2025, https://rsmus.com/insights/tax-alerts/2025/irs-proposes-regulations-to-implement-changes-to-section-162m.html; Crowe, “IRS Proposes new Section 162(m) Regulations,” Mar. 6, 2025, https://www.crowe.com/insights/tax-news-highlights/irs-proposes-new-section-162m-regulations.

[24] Joint Committee on Taxation, “Description of the Tax Provisions of the Chairman’s Amendment in the Nature of a Substitute to the Budget Reconciliation Legislative Recommendations Related to Tax,” May 12, 2025, https://www.jct.gov/publications/2025/jcx-21-25/.

[25] Andrey Yushkov and Katherine Loughead, “State Individual Income Tax Rates and Brackets, 2025,” Tax Foundation, Feb. 18, 2025, https://taxfoundation.org/data/all/state/state-income-tax-rates/.

[26] Such rules are rare in the developed world, with Austria being an exception. See PwC, “Worldwide Tax Summaries,” https://taxsummaries.pwc.com/.

[27] Federal Reserve Bank of St. Louis, “Levels of Wealth by Wealth Percentile Groups,” https://fred.stlouisfed.org/release/tables?eid=813668&rid=453.

[28] Department of the Treasury, “Revenue Consequences of 162(m),” https://home.treasury.gov/system/files/131/Firms-Exceeding-162m.pdf; Craig Doidge, G. Andrew Karolyi, and Rene M. Stulz, “The U.S. Listing Gap,” NBER Working Paper 21181, May 2015, https://www.nber.org/papers/w21181.

[29] Cristina Enache, “Savings and Investment: The Tax Treatment of Stock and Retirement Accounts in the OECD and Select EU Countries,” Tax Foundation, Feb. 22, 2024, https://taxfoundation.org/research/all/eu/retirement-savings-investment-tax/.

[30] Richard A. Booth, “The Mechanics of Share Repurchases or How I Stopped Worrying and Learned to Love Stock Buybacks,” European Corporate Governance Institute – Law Working Paper No. 650/2022, Jul. 8, 2022, https://papers.ssrn.com/sol3/papers.cfm?abstract_id=4118812.

[31] Alex Durante, “Stock Buyback Tax Would Hurt Investment and Innovation,” Tax Foundation, Aug. 12, 2022, https://taxfoundation.org/blog/inflation-reduction-act-stock-buybacks/.

[32] Kyle Pomerleau and John Ricco, “Should Lawmakers Raise the Stock Buyback Excise Tax?,” American Enterprise Institute, Apr. 30, 2025, https://www.aei.org/economics/should-lawmakers-raise-the-stock-buyback-excise-tax/.

[33] Lawmakers may also be considering cutting corporate taxes in various ways, including by rolling back, to some degree, major TCJA base broadeners such as R&D amortization and the stricter limitation on interest deductions that began in 2022. Lawmakers may also be looking to extend bonus depreciation for equipment, returning it to 100 percent expensing that applied from 2018 until it began phasing out in 2023. These changes, depending on how they are structured, have the potential to strongly boost economic growth over the long run while reducing the corporate tax base and revenue in the short run. House legislation would extend these provisions on a temporary basis, but only partially for R&D expensing (excluding foreign-cited R&D), and in addition allow expensing for certain structures, also temporarily. Unless extended again in the future, these temporary provisions would have no impact on economic growth over the long run.

[34] William McBride, “Picking the Right Budgetary Offsets Key to Tax Reform Success,” Tax Foundation, Mar. 12, 2025, https://taxfoundation.org/blog/tax-offsets-spending-cuts-federal-budget/.

Share this article